How to Value a Pot Stock

(Bloomberg Opinion) -- Cannabis growers have hardly any revenue and their product is still illegal in their most desirable market, the U.S. That’s not stopping investors and corporate giants from spending billions of dollars to take stakes in these companies. They obviously see growth potential. And yet the question remains, how do you even value a pot business?

Altria Group Inc., the U.S. tobacco leader and maker of Marlboro cigarettes, announced in December that it was buying 45 percent of Cronos Group Inc., one of Canada’s growing number of cannabis producers and among the industry’s high-flying stocks. The $1.8 billion transaction left us wondering: How did Altria determine that price? After all, in the period before the deal, Cronos generated sales of less than $4 million – no, that’s not a typo – and certainly no profits. Recreational pot had only just become legal in Canada two months earlier. Altria, a $105 billion market-cap company that rarely does splashy deals, placed immense value on a barely existent business in a nascent market.

The dynamics were the same when Constellation Brands Inc., a beer and liquor conglomerate, spent $3.8 billion to increase its stake in Canopy Growth Corp. earlier in 2018. Canopy’s CEO has said he wants it to become the Google of pot – but he’ll need to add a few more digits to its sales figures.

It’s a tricky thing to gauge the worth of assets that will potentially be highly valuable down the road – but are difficult to quantify just yet. Looking at other industries where this has been the case is helpful. Even if their businesses aren’t perfect comparisons, the method of valuing them can be instructive.

Take the natural-resources space, where the focus is often on non-financial metrics. They include production capacity and tangible assets, such as proved oil reserves – which is to say, how much fuel a producer can likely pump from their land. It can be argued that this is similar to how individual investors already have been gauging cannabis companies, dazzled by how many kilograms can be produced and how many acres of greenhouse they have.

But the downside to this approach for cannabis is that it puts too much emphasis on supply-chain processes that may become commoditized, and a rudimentary focus on capacity doesn’t capture how the early movers in this market can differentiate themselves. The industry’s novelty also distracts from what can be a challenging business from an operational standpoint. For example, Aphria Inc.’s share price increased more than elevenfold over the last five years, but in its latest quarter the business was hamstrung by supply shortages and packaging issues.

A better comparison for cannabis may be the biotechnology space. Deals for drug developers involve big, risky bets on future potential blockbusters. These products may not generate revenue yet, but they aim to address very specific markets and are expected to have an economic moat that wards off competition. For pharmaceuticals, that moat comes from patent exclusivity that prevents copycat versions of a therapy. In some ways, this is what the more advanced cannabis companies are looking to accomplish. They won’t have patents in the same way, but they do aim to create intellectual property and specialized brands that appeal to certain types of customers. And they want to be first to form those customer relationships.

Remember, this market will be far more expansive than simply selling a box of joints. There’s an opportunity to create all sorts of consumer products, and the marketing can vary widely – from wellness drinks and beauty items infused with cannabidiol, or CBD (the part of cannabis that doesn’t deliver a high), to “sin†products like marijuana-infused edibles, or something more akin to having a glass of wine.

Look at it this way: Altria doesn’t own tobacco farms. It owns high-margin brands that source from tobacco growers. So when it’s studying the future of marijuana, it’s not looking solely at production. It’s looking for unique brands that can be scaled up by a team with the necessary know-how. In the case of Cronos, CEO Mike Gorenstein said on the last earnings call that the company is trying to differentiate itself with pre-rolled joints, adding that innovation around branding and efficiency will be “a bigger differentiator than just cultivation.â€

Knowing the important role that brand-building will play in the next phase of the cannabis industry’s growth story, it’s useful to study these companies’ senior management teams and look for branding and retail pedigree. It’s a good sign that Cronos’s head of marketing has had stints at PepsiCo Inc. and Mondelez International Inc., and that Tilray Inc. has a one-time Starbucks Corp. executive running its retail strategy.

Green Growth Brands Inc., based in Ohio and Ontario, has a deep bench of such leaders: Its CEO is Peter Horvath, a former executive at American Eagle Outfitters Inc., Victoria’s Secret and DSW. His key deputies come from the likes of Abercrombie & Fitch Inc. and Bath & Body Works. They are rightly emphasizing that retail expertise is a point of distinction and an advantage as they develop targeted brands such as Green Lily, aimed at women, and Camp, aimed at active, outdoorsy types. This brand-centricity seems to be paying off: Even though Green Growth doesn’t have as large a market capitalization as the Canada-based players, it recently scored a partnership with Simon Property Group Inc. to open more than 100 CBD stores in the mall giant’s shopping centers, and its CBD products will be sold in 96 DSW locations.

That U.S. footprint might do it good down the road, as wider marijuana legalization seems likely. While much of the focus these days is around the promise of the Canadian market, it’s important not to let that obscure what should be the cannabis world’s real end game.

And, in general, the Canadian companies that have received such bountiful investor buzz are at something of a disadvantage on the branding front, notes Bethany Gomez, a cannabis industry analyst at Brightfield Group. Because of strict rules in Canada regarding logo size and other packaging details for currently available cannabis products, they are simply limited in how distinctive they can make their presentation.

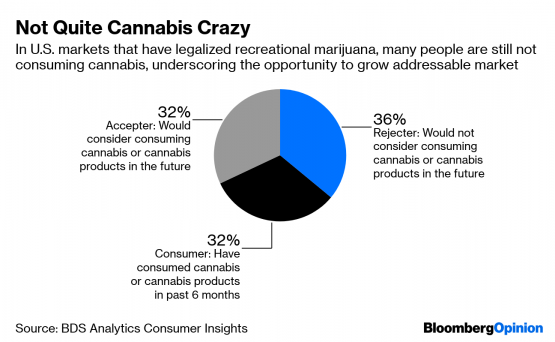

Wherever it’s sold, if the cannabis business is to grow as big as the industry’s bulls hope, it is going to have to successfully court non-users and infrequent users. That’s where newer innovations, such as edibles and beauty items, may be more important than smokeable products.

The companies that become the breakout stars in the legal cannabis era will be the ones that have a vision for how to create demand for such goods, whether through curiosity-inducing product, a great in-store experience or alluring marketing. These capabilities – not merely spreading more seeds in soil – should be a critical part of valuing the pot pioneers.

To contact the authors of this story: Tara Lachapelle at [email protected] Halzack at [email protected]

To contact the editor responsible for this story: Beth Williams at [email protected]

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tara Lachapelle is a Bloomberg Opinion columnist covering deals, Berkshire Hathaway Inc., media and telecommunications. She previously wrote an M&A column for Bloomberg News.

Sarah Halzack is a Bloomberg Opinion columnist covering the consumer and retail industries. She was previously a national retail reporter for the Washington Post.

For more articles like this, please visit us at bloomberg.com/opinion

©2019 Bloomberg L.P.