Energy Transfer Delivers Record Results in Q1

Energy Transfer's (NYSE: ET) significant investments to expand its midstream footprint continued paying dividends during the first quarter. Those growth projects provided the energy infrastructure company with the fuel to produce record earnings and cash flow during the period, enabling it to easily support its 8.1%-yielding distribution. That allowed the company to reinvest its excess cash into more expansions, which should drive continued fast-paced growth in the coming years.

Drilling down into the results

|

Metric |

Q1 2019 |

Q1 2018 |

Year-Over-Year Change |

|---|---|---|---|

|

Adjusted EBITDA |

$2.8 billion |

$2.0 billion |

39.7% |

|

Distributable cash flow (DCF) |

$1.66 billion |

$1.2 billion |

38.6% |

|

DCF per unit |

$0.63 |

$0.47 |

34% |

|

Distribution coverage ratio |

2.07 times |

1.68 times |

23.2% |

Data source: Energy Transfer.

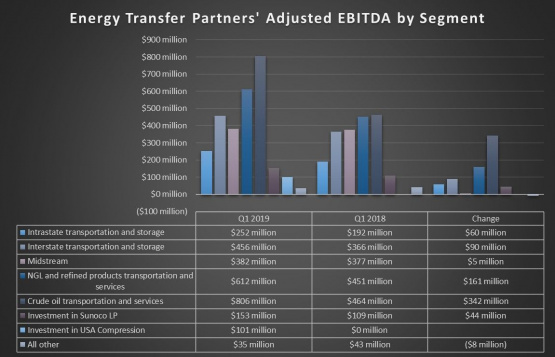

As expected, Energy Transfer's earnings and cash flow rocketed nearly 40% compared with the year-ago period. Not only did the company benefit from expansion projects completed over the past year, but also from its acquisition of a stake in USA Compression Partners (NYSE: USAC), as well as an improvement in the energy market. Those factors helped fuel growth across nearly all its business segments:

Data source: Energy Transfer. Chart by the author.

While all but one of Energy Transfer's business units grew earnings during the first quarter, the biggest contributor was crude oil transportation and services. Earnings in that segment zoomed nearly 74% year over year, thanks to higher volumes flowing through its Texas crude pipeline system as a result of rapidly rising production in the Permian Basin, as well as its recently expanded Bakken Pipeline out of North Dakota. The company also benefited from its ability to buy oil in those two price-constrained areas and move that crude to its Nederland terminal on the Gulf Coast, where it sold for higher prices.

Another major contributor during the quarter was the NGL and refined products business, where earnings surged more than 35%. The company benefited from higher volumes on its Texas NGL pipelines, thanks to the Permian and the ramp-up of the recently completed Mariner East 2 Pipeline. Energy Transfer also completed two new NGL fractionators over the past year, which enabled it to process additional barrels.

Energy Transfer also benefited from its investments in Sunoco LP (NYSE: SUN) and USA Compression. Sunoco LP's strategy to focus on fuel distribution paid off by helping reduce operating expenses, which boosted its profitability. Meanwhile, Energy Transfer gained control over USA Compression last year when the company sold its compression businesses to that entity. That sale is the main reason why earnings in the "all other" segment declined year over year, since Energy Transfer used to report its compression-related earnings in that bucket.

Image source: Getty Images.

A look at what's ahead

Energy Transfer's strong showing during the first quarter has it on track to achieve its full-year guidance. At the midpoint, the company would generate $10.7 billion of adjusted EBITDA, which would be 12.5% above last year's level.

Driving that view is the continued strength of the oil market this year, as well as the company's expansion program. The company continues to place new assets into service, including recently finishing the second phase of the Bayou Bridge pipeline. Meanwhile, the company has more on the way, including an expansion of the Permian Express pipeline system, which should start up during the third quarter.

Energy Transfer currently expects to invest $5 billion on expansion projects this year. In addition to those already in the backlog, the company continues to make progress on securing new ones. The company is currently working on plans to optimize the Bakken pipeline, which would start up in 2020. It's is also partnering with Sunoco LP to develop a diesel fuel pipeline in Western Texas, which could be in service by year-end. Meanwhile, it continues to make progress on the Lake Charles LNG project, which it could approve next year.

The midstream giant took additional steps to firm up its financial foundation during the quarter. It sold a 30% interest in the Red Bluff Express pipeline to Western Midstream for $92.5 million. The company also completed a $4.21 billion debt exchange and issued $800 million in preferred units. Those moves will lower its leverage ratio, reduce interest expenses, and extend the overall maturity profile of its debt. Finally, the company retained $856 million in cash after paying its high-yielding distribution, which helped finance expansion projects.

Excellent in every way

Energy Transfer delivered exceptional first-quarter results. Earnings and cash flow skyrocketed, which has the company on track for another strong year. Meanwhile, it made progress on not only completing expansion projects but securing new ones. On top of that, the company took additional steps to firm up its financial foundation. This across-the-board success is another reason why income-seeking investors should take a close look at Energy Transfer.

More From The Motley Fool

- 10 Best Stocks to Buy Today

- The $16,728 Social Security Bonus You Cannot Afford to Miss

- 20 of the Top Stocks to Buy (Including the Two Every Investor Should Own)

- What Is an ETF?

- 5 Recession-Proof Stocks

- How to Beat the Market

Matthew DiLallo has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.